May 2023 Market Update

Well in the last month there has certainly been enough going on to keep a property investors head spinning. We’ve had the OCR ratchet up another 50 basis points, a bold step in the eyes of many, the Reserve Bank has also released the frame work for debt-to-income restrictions. The Bank is proposing to lift the limit on loans, with LVRs above 80%, for owner occupiers to 15% of the banks’ new lending. For investor loans, from June 1, banks would be allowed to lend 5% of their new loans to investors with less than 35% equity.

The 10-year bright line extension was passed last week under urgency. Post 1 April, interest payment tax deductions are restricted to 50%, as part of the staged non deductibility and the last sneaky wee one is a proposed change to rent increases.

It feels like only yesterday, the law restricting rent increases to once per year had been introduced. The Government is now proposing to limit rent increases to once every 12 months per rental property (not tenancy). This means that if you were to re-let the property to new tenants, you would be restricted to lift the price up, if it had not been 12 months since the last rent increase.

The Government is still considering further changes - removal of interest-only loans on investment properties, the introduction of debt-to-income caps, rent controls and allowing interest deductibility for new builds. These will be reviewed this month.

Allowing for all of the above you’ll appreciate why many investors are holding their chips and waiting to see what this election year is going to deliver.

The economy shrank 0.6% in the final three months of last year, Stats NZ has announced. It also revised down its estimate of growth in the previous September quarter to 1.7%, from its original estimate of 2% growth. The fall in GDP in the three months to the end of December was larger than any of the major banks had been forecasting. Prior to Stats NZ’s announcement, ASB had been forecasting GDP would decline 0.5%, with the other four major banks predicting drops of either 0.2% or 0.3% after some late downward revisions.

The drop means the Reserve Bank may have got the recession it has been attempting to engineer about six months earlier than it had expected. The Reserve Bank predicted at the time it released its latest monetary policy statement last month, that GDP had grown 0.7% in the December quarter and would rise by a further 0.2% during the current quarter before entering a shallow nine-month recession.

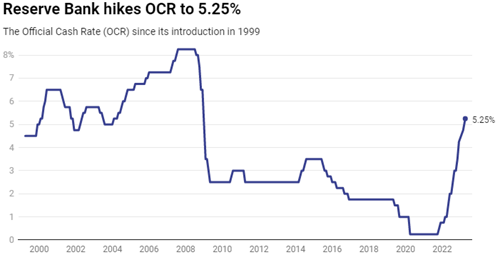

Annual inflation has plummeted to 6.7%, after prices rose only 1.2% in the three months to the end of March. The drop in inflation was much larger than economic forecasters had been expecting and may raise questions over whether the Reserve Bank may have been engaging in “overkill” when it raised the official cash rate by 50 basis points to 5.25% earlier this month.

Is the Property Market Near the bottom?

The housing market downturn could be nearing its end, with the latest figures showing key indicators are not as weak as they have been, CoreLogic says. House prices continued to fall, with a 2.4% decline nationwide in the March quarter, which took the annual decline to 10.5%, according to the property research company’s latest Housing Chart Pack.

But CoreLogic Chief Property Economist, Kelvin Davidson, said price falls were easing, and there were green shoots beginning to emerge among metrics such as sales volumes and listing numbers.

Sales volumes were relatively low, and down 30.9% in the year to March, but there were hints in the figures that the worst might have passed for activity, he said. “We may now be seeing the first signs of a floor. The rate of annual decline has slowed down, and after seasonal adjustment, volumes increased by as much as 10% from February to March.”

There had been little movement among banks and lenders to pass on the Reserve Bank’s 50 basis point increase to the official cash rate in April, he said. “This decision suggests mortgage rates may have reached their peak, allowing borrowers to quantify their ‘worst case’. “Any suggestion that interest rates have topped out will provide buyers and sellers with more confidence and is eventually likely to result in a turnaround in housing sentiment.”

However, Infometrics Chief Executive Brad Olsen says people should be under no illusion the inflation battle is over. Interest rate rises are still to come, he says, even though most of the “heavy lifting” is over. “The Reserve Bank will still not be comfortable with the numbers as they are set and I don’t think they’re done”.

Another Official Cash Rate hike does not necessarily mean higher interest rates for homeowners, though, with increases already priced in. Olsen says according to some measures, house sales are at their lowest since the 1980s, which means banks need to do enough business to keep operating. “That means they won't be nearly as gung-ho with raising interest rates. They might have to wear some of those increases to keep their mortgage book at a big enough level.”

University Goes From Strength to Strength

Last month I mentioned student accommodation was at capacity with the University of Canterbury (UC) being seen as “the cool place to be”. Well, as we move towards the student letting part of the year, we will be keeping a keen eye on what is happening just around the corner from our Fendalton office. It’s a record year for enrolments at UC.

As of late March, 21,361 students have enrolled at Canterbury, up from 20,223 at the same time last year. As the new term got under way, UC had 19,975 domestic students, while the international headcount was 1,393 – the latter rising from 1098 the year before.

Early this month, UC held its first city centre graduation procession for three years. The special parade – or “procesh” – was the first time UC students have taken to the streets in their mortar boards and gowns since 2020.

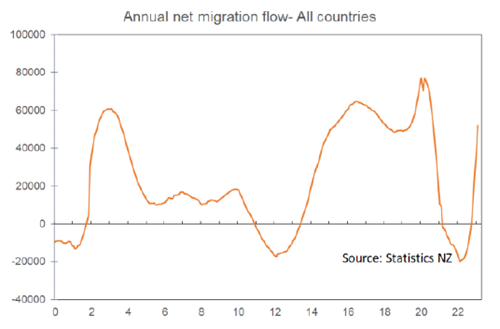

Migration Boom

No-one expected that in the year to February the net migration gain would be 52,000 as compared with a loss of 20,000 a year ago. This has taken us all by surprise along with the better ability for Kiwis in Australia to gain citizenship we now have a potential population-sapping brain drain. Very little focus has been on the already soaring net inflows which may be bringing some improvement in business ability to find staff, again this will add pressure to the housing market that is already at near breaking point.

And to the Local Market

Again, this month the numbers have been up and down a little with regard to the number of properties available across the city. Today we sit at 686 up from 639 at the close of last month. The additional 50 or so hasn’t had any effect in real terms on the supply and demand point of view.

At the time of writing, Trademe was yet to put out its property report for April but from what we have seen there has been no let-up in rents across the city as supply still remains tight. Winter markets often feature subdued tenant enquiry rates, April saw a total of 42 tenancies signed in the office, down from 65 for March and 56 for February. It will be interesting to see next month if the winter renting blues are starting.

What’s popular this month? Four bedroom properties under $600pw - no surprises there, properties of that scale are seldom under $600pw now. Three bedroom, two bathroom properties with a garage are the next cab of the rank. Our furnished options have also been doing well this month with all but one available having been rented. It’s a different demographic that seeks a furnished property but as I like to say there is a property for everyone.

It's Not All Doom and Gloom

Christchurch is truly a vibrant, fun city that’s affordable compared to other parts of NZ. If you’re in the property game then the aim is to ride the wave, the turbulence we are feeling right now is just part of the 10 year property cycle and we have been here many times before and come out well in the end. We are inundated with new managements a sign that investors are still buying in Christchurch. There are many projects yet to be completed in the city which will add to the drawcard so all-in-all I feel we are sitting in a good position to see out any turbulence the market and central Govt. want to throw at us.

A few last throw away stats because I enjoy them -

- Population of New Zealand as at 31 December 2022: 5,151,600

- As at 31 March 1991 the New Zealand population was: 3,488,000

- An increase over the 31.75 years of: 1,663,600

- An average increase of: 52,397 per year (it is no wonder we have a housing issue

As always, we do truly appreciate your business and the team and I are always just a phone call away. We are always available for a free chat and are happy to share our experience and knowledge wherever we can be helpful.

Hamish and the Team @A1